Our client, a US biased leading jobs recruitment platform, was scaling fast across international markets, but its payment infrastructure was quietly creating risk it couldn’t see.

There’s a particular kind of operational problem that doesn’t announce itself loudly. It doesn’t crash systems or trigger alarms. It just accumulates, in spreadsheet tabs that grow longer every month, in analyst hours spent cross-checking numbers that should already match, in overcharges that slip through because nobody had time to catch them.

That was the reality for the finance team at a leading US-based SaaS platform, operating across multiple markets in the US and EU. The company ran its payment stack across seven different processors, each with its own reporting format, its own fee structure, and its own logic. Seventy-seven integrations in total. All of it landed on the desks of a three-person team and their manager, armed with Excel.

The problem nobody could see all at once

The finance team wasn’t struggling because they were disorganized. They were struggling because the data itself was fragmented by design. Each processor reported differently. Comparing fee structures across partners meant manually translating one set of numbers into another before any analysis could even begin. In the team’s own words: they couldn’t “compare apples to apples.”

Fee validation alone consumed more than ten hours every week. Tier-based pricing models, where rates shift depending on transaction volume, made the work especially unforgiving. A small miscalculation early in the month could cascade quietly into a billing discrepancy that nobody would catch until someone had the bandwidth to dig.

FX issues were worse. Cross-currency charges that deviated from contractual rates were flagged reactively, if at all. The team knew discrepancies were happening. They just didn’t know how often, or how much they were being absorbed silently into the cost base.

The $300,000 moment made it concrete. Before any new tooling was in place, the team discovered a six-figure overcharge through manual review, not through a system, not through an alert, but through sheer persistence. It was a wake-up call. If that one had slipped through, it would have been paid without question.

Reporting added another layer. Financial data lived across disconnected spreadsheets. Before any number could be used, for bookkeeping, for analysis, for revenue recording, someone had to manually consolidate it first. There was no single layer where all processor data was standardized and ready to work with.

Building the foundation

The company came to Simetrik looking for a way to unify its processor ecosystem without ripping it apart. The goal wasn’t to consolidate providers, it was to build a control layer above them, one that could ingest data from all seven processors and surface it in a consistent format.

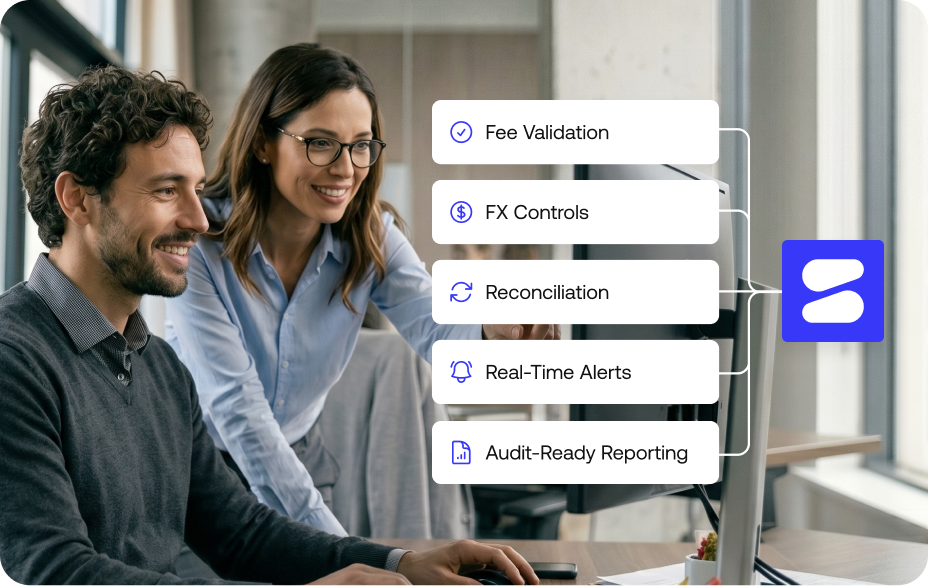

Phase one focused on the fundamentals: consolidating the 77 integrations into a single standardized data layer, automating fee validation, and replacing ad hoc exception handling with proactive controls.

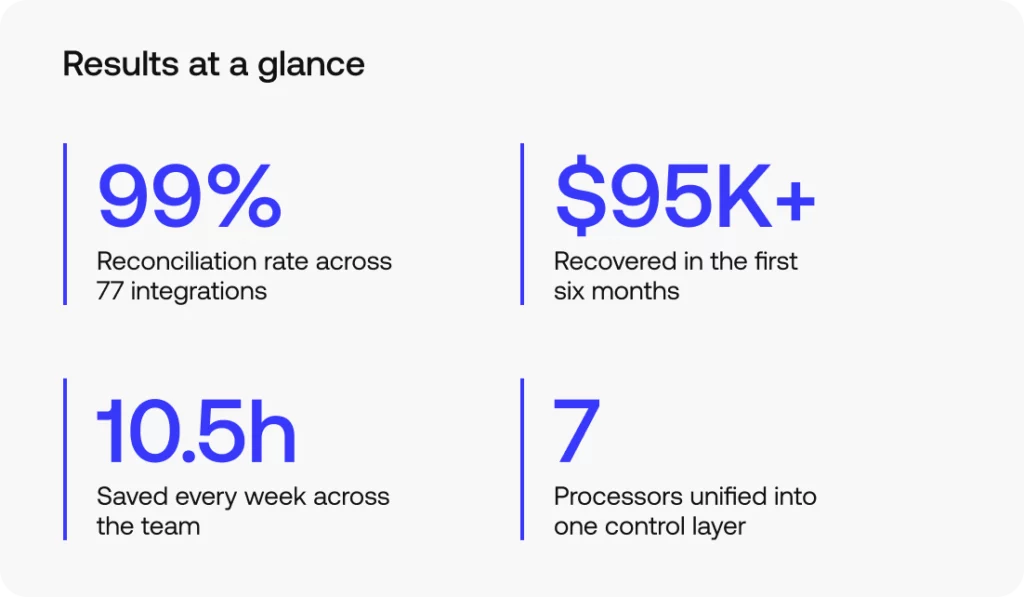

The mapping, transformation, and tier-pricing aggregation that had previously consumed a significant portion of three analysts’ weeks was now handled automatically.. When a processor billed incorrectly, whether due to a rate misapplication, an FX deviation, or a billing error, Simetrik surfaced it. The team stopped discovering overcharges after the fact and started catching them as they happened. Every processed transaction was confirmed and matched against third-party reporting in real time. Giving the team a single number they could trust: a 99% reconciliation rate across the full processor ecosystem.

The financial impact was immediate. In Phase 1 alone, the platform identified six-figure savings from processor overcharges and billing discrepancies. Over the first six months, the team recovered more than $95,000 in overcharged fees and reclaimed more than ten hours of analyst time every week. Each team member got back roughly 10% of their workday.

The broader pattern

There’s a version of this story that happens at nearly every company operating a multi-processor payment stack. The fragmentation isn’t a failure, it’s the natural result of building across markets, adding partners as the business grows, and managing complexity one integration at a time. The problem is that the tools built to handle early-stage complexity don’t scale with it.

Excel is remarkable at what it does. But a three-person team running manual fee validation across seven processors and tier-based pricing models is a system operating beyond its capacity.

What this case illustrates is that the path to financial control in a complex payment environment isn’t simplification. It’s unification. Building a layer that standardizes data across sources, automates the validation work, and surfaces exceptions before they become losses, that’s what turns a fragmented processor ecosystem into something a finance team can actually govern.

The $300,000 overcharge was already hiding in plain sight before Simetrik was implemented. The question isn’t whether there are more like it in your stack. The question is whether you have the infrastructure to find them.

Domains in scope

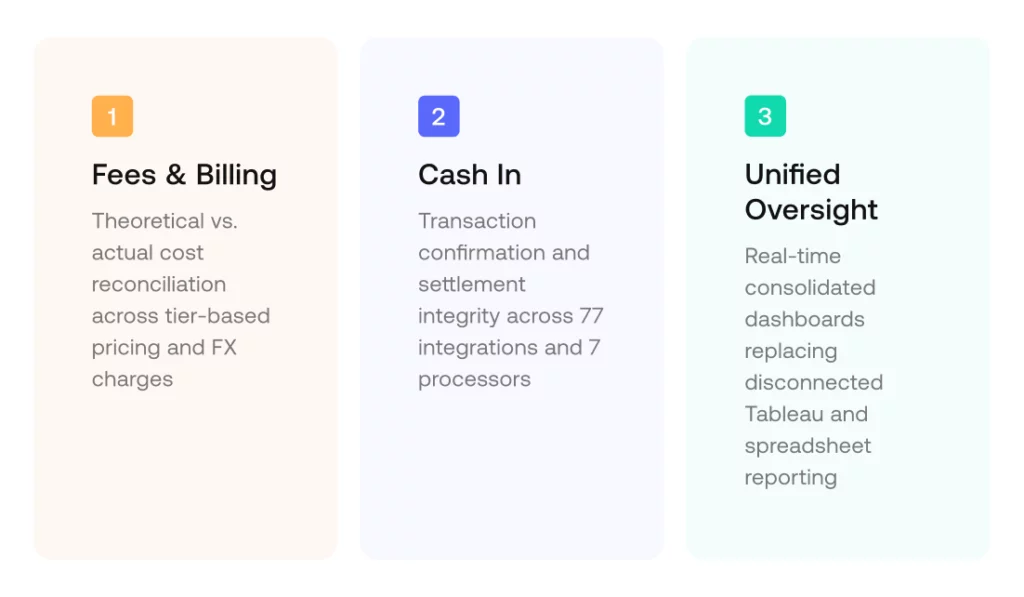

Simetrik organizes financial operations control around eight domains, each one covering a distinct area where money moves, fees are applied, or financial data needs to be trusted. In any given engagement, the domains in scope reflect where a company’s risk actually lives. For this customer, three domains were at the center of the work.

Cash In: Transaction confirmation and settlement integrity controls across 77 integrations, ensuring every processed transaction is accurately confirmed and reconciled against third-party reporting.

Fees & Billing: Theoretical vs. actual cost reconciliation across tier-based pricing structures and FX charges, replacing manual Excel validation across seven processor contracts.

Unified Oversight & Alerts: Real-time consolidated dashboards replacing disconnected spreadsheet reporting, giving finance and treasury leadership a single source of truth across the full processor ecosystem.

Company identity has been anonymized at the client’s request.