For years, your fintech has thrived on a simple formula: build a sleek front-end, acquire users rapidly, and let a traditional sponsor bank handle the heavy regulatory lifting behind the scenes. It’s a model that allows startups to move fast and break things without actually breaking federal banking laws.

As transaction volumes scale, those “training wheels” start to look like expensive roadblocks.

Thanks to the passage of the 2025 GENIUS Act and a wave of pro-innovation rulings under OCC Comptroller Jonathan V. Gould, the window for federal charters is wide open. Following the December 2025 conditional approvals for giants like Ripple, Circle, Paxos, and Fidelity, a flood of small-to-medium fintechs and digital asset firms are now eyeing the OCC National Trust Charter.

Securing an OCC Charter is the ultimate graduation for a scaling fintech. It cuts out the sponsor bank middleman and preempts a patchwork of 50 different state licenses. However, federal examiners do not grade on a curve. If your back office still runs on spreadsheets and manual Python scripts, your application is dead on arrival. An OCC charter is the gold standard of financial regulation. Earning one signals to Wall Street, enterprise partners, and retail consumers that your institution is heavily capitalized, strictly regulated, and built to survive economic downturns.

Here is what it takes to get your operations ready for the federal standard.

The Reality Check: Startup Agility vs. Bank-Grade Compliance

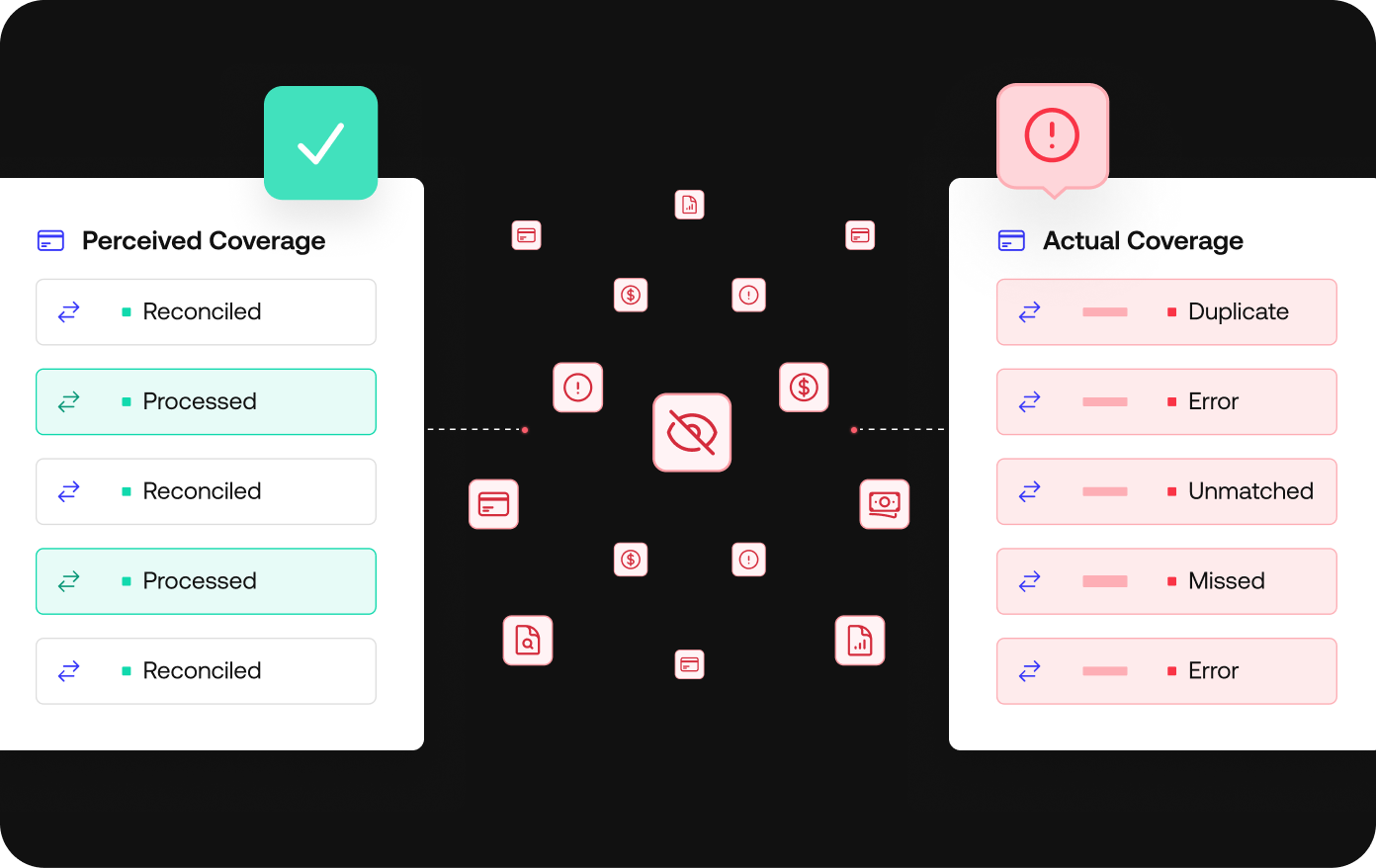

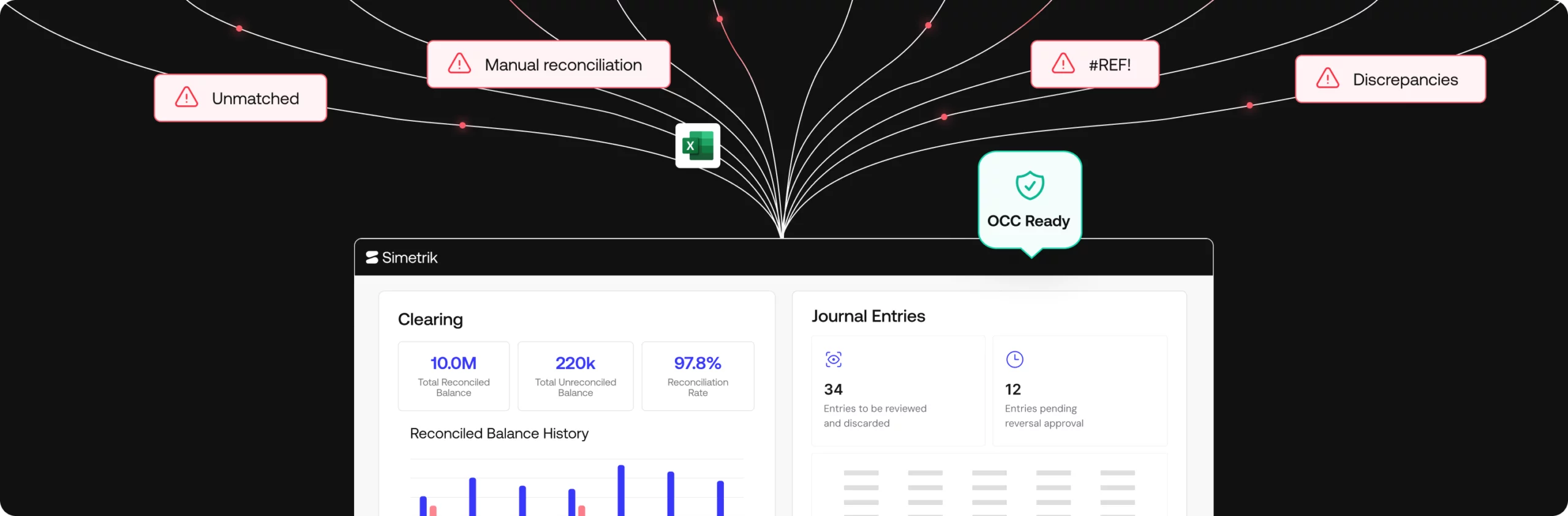

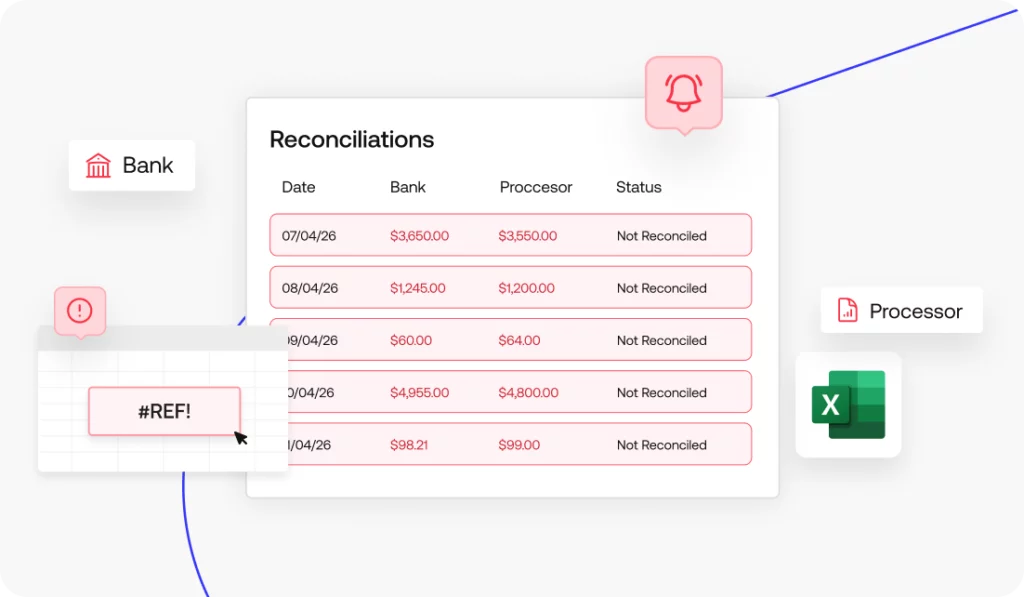

Right now, your finance team probably relies on Excel, Google Sheets, or homegrown Python scripts to match transactions, catch invisible revenue leakage, and run the month-end close. When discrepancies occur, your team manually hunts them down across multiple processor portals.

This is the “good enough” trap. It works when you have 10,000 users, but it breaks when you scale.

The OCC demands “bank-grade safety and soundness.” This means examiners have zero tolerance for operational gaps, delayed settlement tracking, or manual reconciliation errors. You cannot manage billions in fiduciary assets, issue stablecoins, or run a federally regulated payments program using VLOOKUPs. When regulators come knocking, spreadsheets won’t hold up to scrutiny. A proven, auditable system gives you the documentation and traceability to face any regulatory review with confidence.

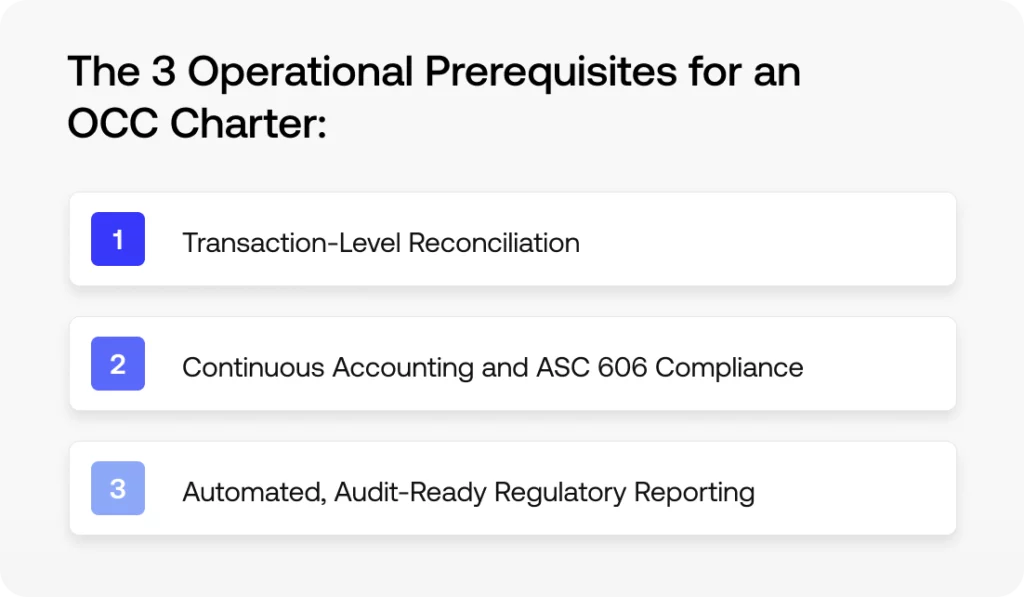

The Three Operational Prerequisites for an OCC Charter

To pass an OCC exam, you must prove that your financial controls are automated, continuous, and foolproof. Here are the three operational pillars you must have in place:

Prerequisite 1: Transaction-Level Reconciliation

Traditional financial close tools are balance-level focused. They are not built to handle the complexity of matching 24/7 crypto trades, volatile network gas fees, and card network chargebacks against fiat ACH and wire rails.

- The Standard: You need continuous, automated, transaction-level reconciliation.

- How Simetrik Solves It: Simetrik aligns operations data for all product operations, such as payment processing, ATMs, and other digital products, with accounting records daily, tracking every single dollar from the payment processor to the core ledger. We automate discrepancy detection within 24 hours, preventing the 5 to 15 basis points of invisible margin leakage that usually slips past manual reviews.

Prerequisite 2: Continuous Accounting and ASC 606 Compliance

If your month-end close takes 8 to 12 days because your team is bogged down by manual journal entries and spreadsheet-based revenue recognition, regulators (and investors) will see a massive red flag.

- The Standard: A continuous, highly automated close process that is perpetually audit-ready.

- How Simetrik Solves It: Simetrik automates revenue recognition directly from transaction-level payment data, ensuring strict ASC 606 compliance. By systematically generating journal entries for revenues, fees, and provisions, we reduce manual journal entries by 80%+. The result? A 2-3 day close with zero posting errors.

Prerequisite 3: Automated, Audit-Ready Regulatory Reporting

Compiling FinCEN, BSA/AML, and SOC 2 reports manually takes weeks of engineering and compliance resources, leaving massive room for human error. Under the OCC, these reporting requirements become heavier and more frequent.

- The Standard: Complete transaction-level audit trails that can be generated on demand for federal examiners.

- How Simetrik Solves It: We transform compliance from a manual burden into automated assurance. Simetrik generates FinCEN, AML, and other required regulatory reports directly from your transaction data, maintaining SOC 2-ready controls while reducing your overall compliance costs by up to 60%.

Stop Acting Like a Tech Company, Start Operating Like a Bank

You need Unified Oversight. Executives must have real-time KPIs across all product operations, from cash positions across funding sources to proactive anomaly alerts, with the ability to drill down from a summary dashboard straight to the transaction level. When the OCC (or your board) asks a question about unit economics or funds flow integrity, you must be able to answer it with instant, verified data.Are you preparing your operations for the next stage of scale?

Schedule a 30-minute personalized demo with Simetrik.

We’ll use a secure sandbox environment with either dummy data or your actual payment data to show you live, automated discrepancy detection and the regulatory-grade audit trails required for federal compliance.