Every fintech CFO has the same answer when you ask about reconciliation: “We’re covered.”

The dashboards are green. The month-end close completes on schedule. The board deck shows transactions processed, revenue recognized, and cash positions balanced. Everything looks healthy.

And then someone finds $2 million in losses that was there the entire time.

This is what we at Simetrik call the Confidence Gap, the distance between what finance leaders *believe* their reconciliation covers and what it *actually* covers. It is the most expensive blind spot in modern financial operations, and it is growing wider as payment complexity accelerates.

The Anatomy of an Invisible Problem

The Confidence Gap does not announce itself. There is no failed reconciliation run, no red flag in the dashboard, no alert from your payment processor. The numbers check out at the level you are looking at. The problem is that you are looking at the wrong level.

Consider a real case: a sophisticated payment processor operating across three markets, processing billions in annual volume. They had reconciliation processes. They had a finance team. They had dashboards. And buried inside their data were three separate sources of margin leakage totaling $2 million. None of which were visible to their existing controls.

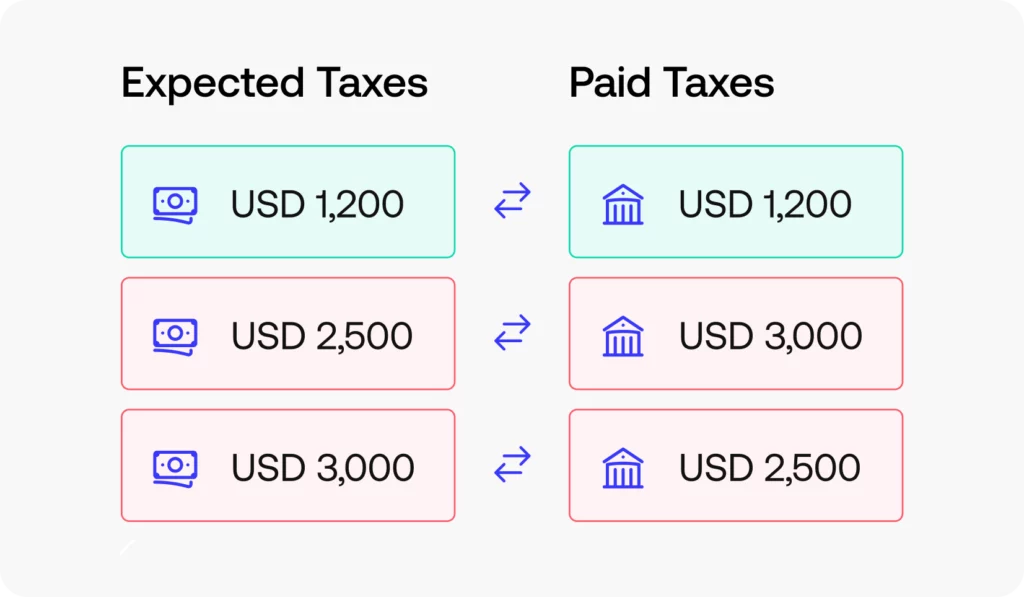

The first was a partner bank incorrectly withholding taxes on transactions. At the aggregate level, “taxes paid” checked out. At the transaction level, the wrong taxes were being applied to the wrong transactions. The second was a transaction code ambiguity, multiple acquirers used the same code for refunds and chargebacks, causing missed dispute deadlines and absorbed losses. The third was a pattern of duplicate debits on refunds spanning multiple countries, invisible without cross-entity pattern detection.

These were not edge cases. They were systemic, ongoing losses hiding behind reconciliation processes that looked perfectly functional.

Three Forces That Widen the Gap

The Confidence Gap is not caused by negligence. It is a structural consequence of three forces that compound as fintechs scale.

Volume masks discrepancies

When you process millions of transactions, aggregate numbers look healthy even when errors are accumulating underneath. A $500 tax misapplication on one transaction is noise. That same error compounding across thousands of transactions over months becomes a seven-figure problem, and it never triggers an alert because the totals still balance within acceptable thresholds.

Complexity outpaces process

Every new payment method, every new market, every new banking partner adds reconciliation complexity. Your team bolts on new processes to handle the new flows, but those processes were designed for yesterday’s architecture. The result is a growing patchwork of manual reviews, spreadsheet cross-references, and scripts that work until they silently stop.

Reconciliation is treated as hygiene, not infrastructure

It gets investment last, attention last, and talent last. Your best engineers are building product features, not reconciliation pipelines. Your best analysts are preparing board decks, not investigating transaction-level anomalies. Reconciliation gets treated as a back-office checkbox until a regulator, an auditor, or a $2 million loss forces it into the spotlight.

The Regulatory Signal You Cannot Ignore

If the business case alone does not close the gap, the regulatory environment should.

In late 2024, the FDIC proposed a new recordkeeping rule for custodial accounts. This was a direct response to the Synapse Financial Technologies collapse, which left over 100,000 consumers locked out of their money and exposed an estimated $65 million to $95 million shortfall between bank records and actual customer balances. The proposed rule pushes banks partnering with fintechs toward transaction-level traceability of beneficial ownership. A standard that makes aggregate reconciliation insufficient by design.

While the rule’s timeline has shifted under the current administration, the direction is clear: regulators are moving toward requiring the granularity that most fintech reconciliation architectures were never built to provide. Whether the FDIC rule takes effect this year or not, the expectation of transaction-level auditability is becoming the baseline. Companies that get ahead of it will have a competitive advantage; companies that wait will be scrambling.

Five Warning Signs You Have a Confidence Gap

Not every company has a $2 million problem. But most scaling companies have at least two of these five warning signs and if you recognize more than two, the gap is real.

Your reconciliation runs on a schedule, not on events

End-of-day or twice-a-week reconciliation creates windows where errors compound undetected. Event-triggered reconciliation catches a $500 error on day one. Batch reconciliation discovers a $500,000 problem six months later.

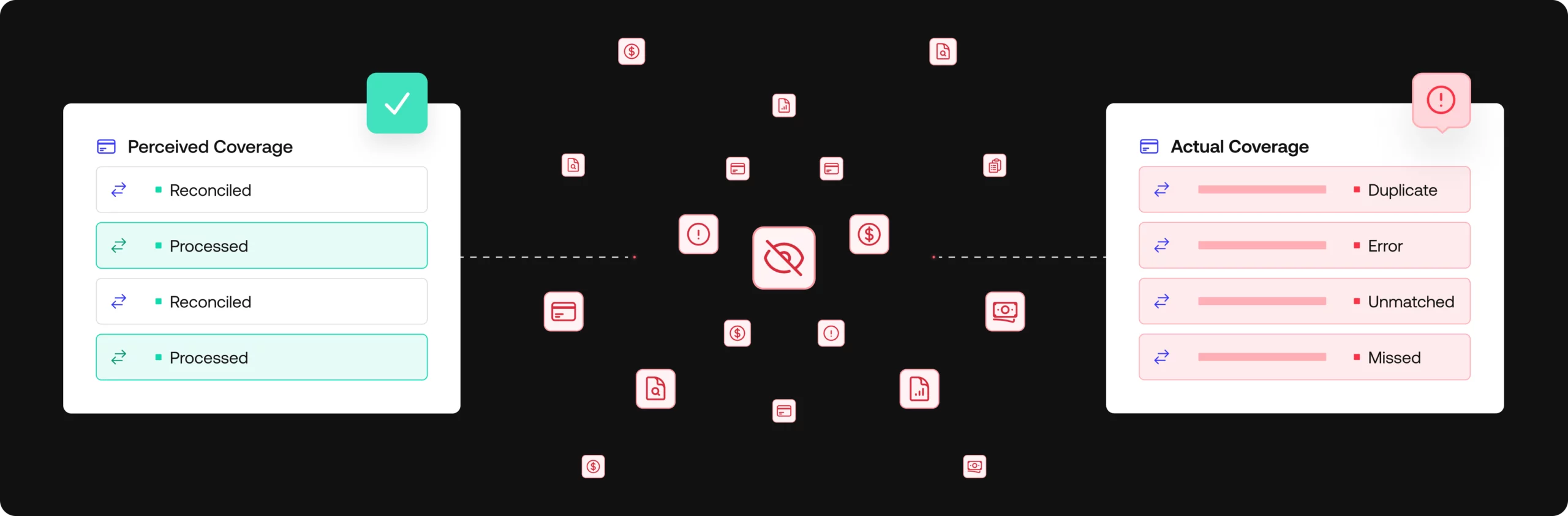

You reconcile in aggregate, not at the transaction level

The $470,000 tax issue described above was invisible at the aggregate level. “Taxes paid” checked out. “Correct taxes paid on correct transactions” did not. If your reconciliation summarizes before it compares, it is designed to miss the errors that matter.

Your reconciliation is siloed by partner or market

The duplicate-debit pattern spanned three countries and multiple acquirers. No single partner’s data showed an anomaly. Only a cross-entity view comparing behavior patterns across all acquirers simultaneously could surface it. If your reconciliation runs in parallel silos that never intersect, cross-entity patterns stay invisible.

Finance cannot configure a new reconciliation flow without engineering

In the case study above, the company went from six weeks to two weeks to onboard a new payment method once finance could configure flows independently. When reconciliation depends on engineering backlogs, your speed to market is bottlenecked.

A regulatory audit would take you weeks, not hours

If producing a complete transaction-level audit trail is a project rather than a query, your infrastructure lacks the granularity you think it has. As regulators push toward real-time traceability, “we can get it to you by next week” is not going to be an acceptable answer.

Closing the Gap

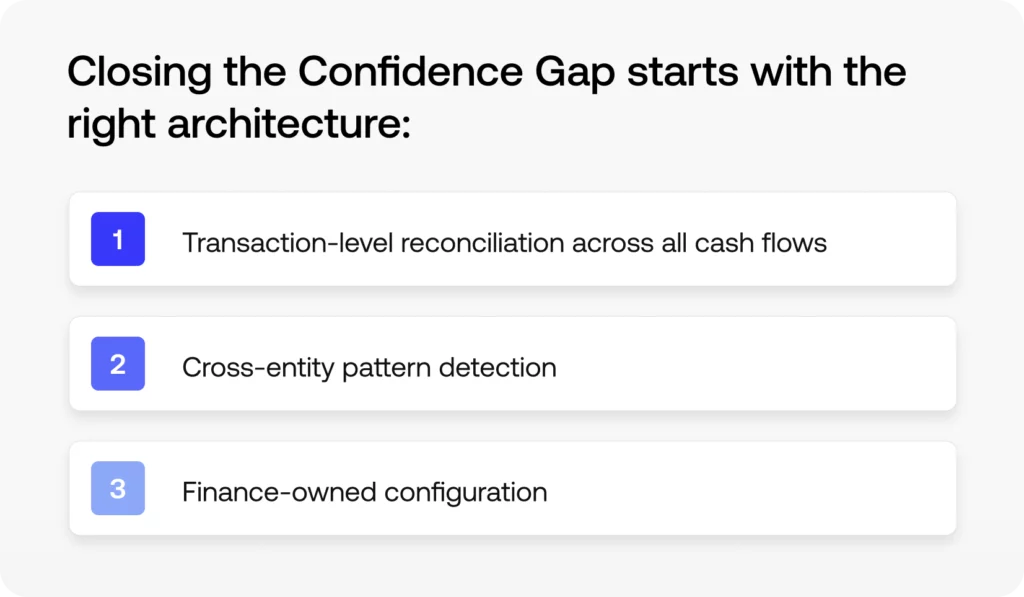

The companies that close the Confidence Gap share three architectural characteristics;

Transaction-level reconciliation across all cash flows

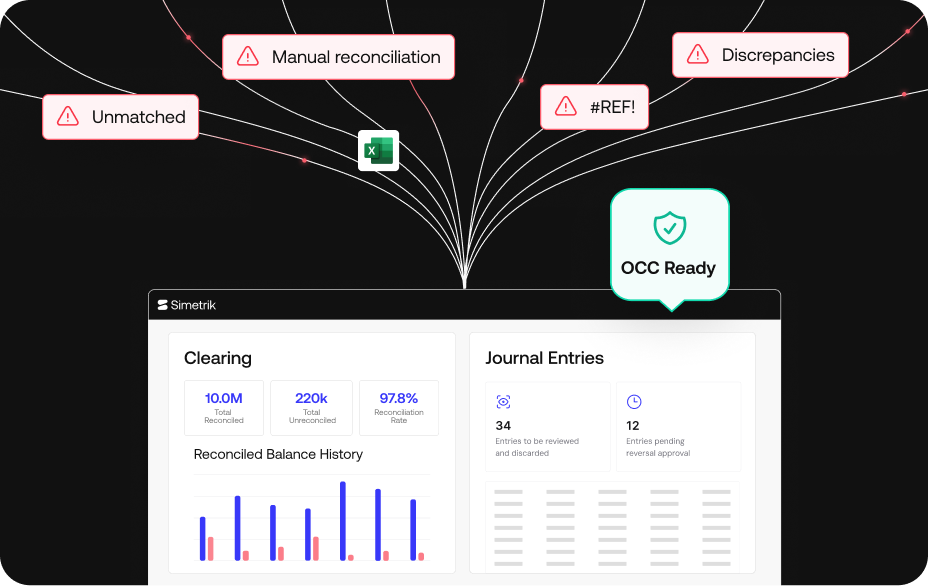

Not summary batches, not aggregate totals, but every individual transaction matched from payment processor to core ledger, continuously. Simetrik automates this across all inbound and outbound payment flows, reconciling at the transaction level and flagging discrepancies within hours, not weeks. This is how the $470,000 tax phantom was found: by comparing individual transactions against banking records instead of trusting aggregate totals.

Cross-entity pattern detection

Discrepancies that span multiple partners, markets, or acquirers require a unified view of all settlement data. Simetrik’s platform processes 2.5 billion records daily across 50+ countries, enabling the kind of cross-entity anomaly detection that caught the duplicate-debit pattern across three markets. Manual processes and siloed reconciliation tools are structurally incapable of surfacing these patterns.

Finance-owned configuration

When finance teams can build and modify reconciliation flows without waiting for engineering, two things happen: new payment methods get reconciled from day one (instead of six weeks later), and the people closest to the business logic are the ones designing the controls. Simetrik’s no-code platform puts reconciliation configuration in the hands of finance and ops teams, reducing dependency on engineering.

Do you have gaps?

The Synapse collapse proved that a company can process billions in volume, serve millions of customers, and still lose track of tens of millions of dollars because of a visibility failure. Their reconciliation architecture was not designed for the complexity they had grown into.

The $2 million case study proves that even sophisticated processors with real reconciliation processes can have systemic margin leaks hiding in plain sight.

The question is not whether you have a Confidence Gap. The question is whether you will close it before it costs you more than you are comfortable discovering.

Are you ready to see what your current reconciliation is missing? Schedule a 30-minute personalized demo with Simetrik. We will use a secure sandbox environment with either dummy data or your actual payment data to show you live, automated discrepancy detection and the transaction-level audit trails that close the gap.